Global Poultry Industry: A Market Analysis

The poultry sector has undergone major structural changes during the past two decades due to the introduction of modern intensive production methods, genetic improvements, improved preventive disease control and biosecurity measures, increasing income and human population, and urbanization. These changes offer tremendous opportunities for poultry producers, particularly smallholders, to improve their farm income. Evidence from case studies shows that it is difficult to see a bright future for smallholder poultry production in a rapidly changing industry structure; however, smallholders can still compete with larger producers with savings that smaller units can achieve because of foregone or cheaper overheads, lower labour costs per unit and, possibly, more intensive supervision, leading to relatively high-profit efficiencies.

Smallholders also have problems meeting high demands for food safety, traceability and compliance, because of high coordination costs and high transaction and marketing costs. Increasingly it appears that smallholders’ ability to maintain their competitiveness in these types of markets is dictated by their ability to establish market trust and reputation along the marketing and distribution channels.

Introduction: Changes in the structure of the poultry sector in developing countries

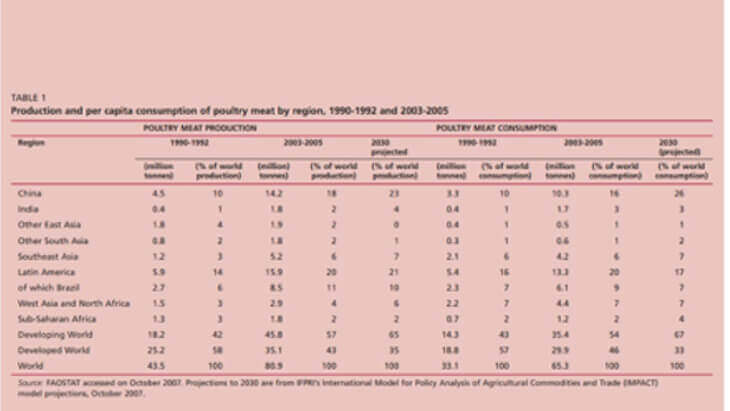

Over the last four decades, there has been rapid growth in livestock production and a rapid change in how animal products are produced, processed, consumed and marketed. Growth in livestock production in both developed and developing countries has been led by poultry. From the 1990s to 2005, consumption of poultry meat in developing countries increased by 35 million tonnes – almost double the increase that occurred in developed countries.

The increase in poultry meat consumption has been most evident in East and Southeast Asia and in Latin America, particularly in China and Brazil. The share of the world’s poultry meat consumed in developing countries rose from 43 to 54 percent between 1990 and 2005, which accounted for 36 percent of the large net increase in meat consumption in developing countries over this period. Further, the proportion of the world’s poultry meat produced in developing countries rose from 42 to 57 percent. It is estimated that production and consumption of poultry meat in developing countries will increase by 3.6 percent and 3.5 percent, respectively, per annum from 2005 to 2030 because of rising incomes, diversification of diets and expanding markets, particularly in Brazil, China and India.

Image source: http://fs-1.5mpublishing.com/images/global_poultry_trends/table1_05-09-13.jpg

The trends described above, and our current knowledge of smallholder involvement, raise a critical issue: for once, a sector in which the poor are heavily involved is growing. In fact, pork and poultry are the prominent growth sectors of developing-country agriculture. If the poor fail to remain active or participate in this sector, they will miss a tremendous opportunity to improve their livelihoods. If they participate, farm income could rise dramatically; however, the conditions under which this could occur are unclear. Although the above-mentioned issues are real, it has also been suggested that the principal reason for the exit of smallholders from livestock production in developed countries is that they are not competitive enough, with the larger operations that benefit from both technical and allocative economies, embodied in genetic improvement of animals and feeds or improved organization – especially in the case of poultry and pig production where profitable adoption simply requires larger farm sizes. This is a particularly difficult issue for smallholders, as it conveys a sense of inevitable economic doom propelled by technological progress. Most livestock production experts do not look much beyond this explanation when assuming the inevitability of livestock industrialization in developing countries. In this reading, we try to disentangle the issues and provide empirical evidence drawing on case studies, involving household surveys, which capture various factors affecting profitability, including transaction costs and efforts to mitigate environmental externalities, for different sized producers in a number of countries.

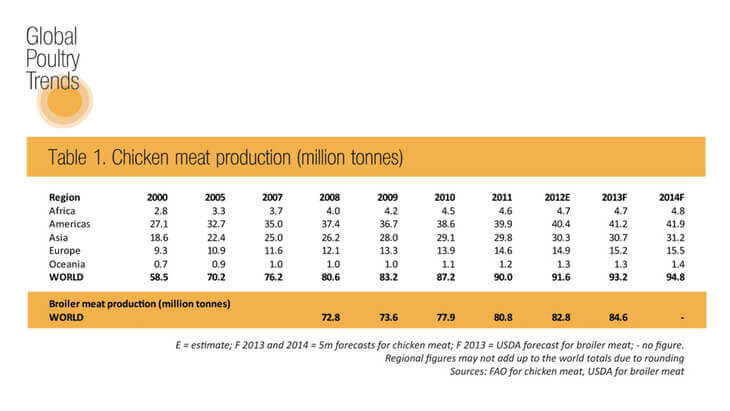

1. Demand-side factors affecting the global poultry sector: Growth of the poultry industry has been both demand and supply driven. The factors that can cause the demand curve to shift are: (1) increases in income; (2) increases in the price of poultry substitutes such as pork or beef; (3) increases in the preference for poultry; and (4) decreases in the price of poultry complements. Factors influencing this shift are growth in population, increases in real per capita incomes, income elasticity of demand, urbanization and variations in real prices. Additionally, in many countries, the population’s tastes and preferences for food products are changing, resulting in a shift away from “inferior” goods towards those considered “superior”. The regions where annual income growth rates are highest, such as Africa (4.2 percent), Asia (3.5 percent) and Latin America (2.3 percent), are also those where the population growth rates are highest (between 1.2 percent and 2.2 percent)

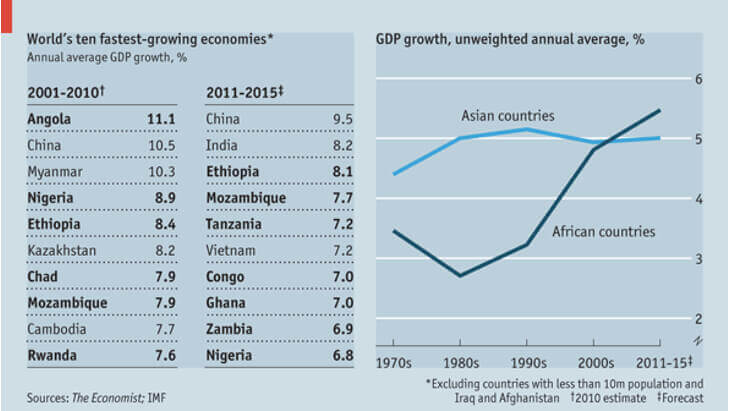

Image source: https://cdn.static-economist.com/sites/default/files/20110108_WOC856_0.gif

Image source: http://www.thepigsite.com/articles/contents/13-08USDAAg1.gif

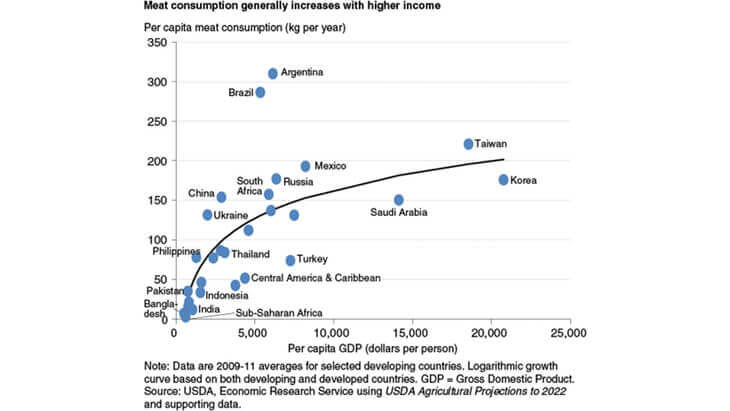

As income increases, meat consumption tends to increase. High expenditure elasticity in poultry indicates its dominance in the diet both in the developed and the developing world. There is generally a positive relationship between per capita consumption of poultry products and per capita incomes. This positive relationship supports the general economic theory which suggests that as incomes increase, particularly in developing countries, people will increase their consumption of high income-elastic food. Throughout the world, this shift has traditionally involved the substitution of meat for starches. This additional meat can be produced either domestically by the reallocation of resources or by import.

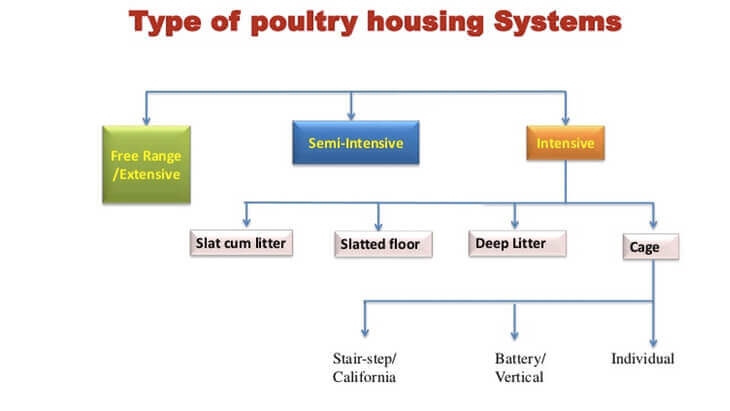

2. Supply-side factors affecting the global trends of the poultry sector: Technology change in the poultry industry has been very rapid. The move from free-ranging to confined poultry operations dramatically increased the number of birds that one farmer could manage.

Image source: https://image.slidesharecdn.com/seminar-140625012659-phpapp01/95/poultry-housing-system-5-638.jpg?cb=1499229715

This shift facilitated the substitution of capital for labour in animal production, and led to a significant increase in labour productivity. Technology change in the poultry industry, led by advances in breeding that improved animal size, fecundity, growth rate and uniformity, has enabled farmers to increase output per unit of feed, produce more birds per year, improve animal disease control and decrease mortality. In terms of management techniques, the move to enclosed production systems in which animals of different ages are segregated and raised apart has had a positive impact on disease control.

Image source: https://i.pinimg.com/736x/10/c5/a0/10c5a0d52d60aa66db5cf43d088b47ab–poultry-house-chicken-cages.jpg

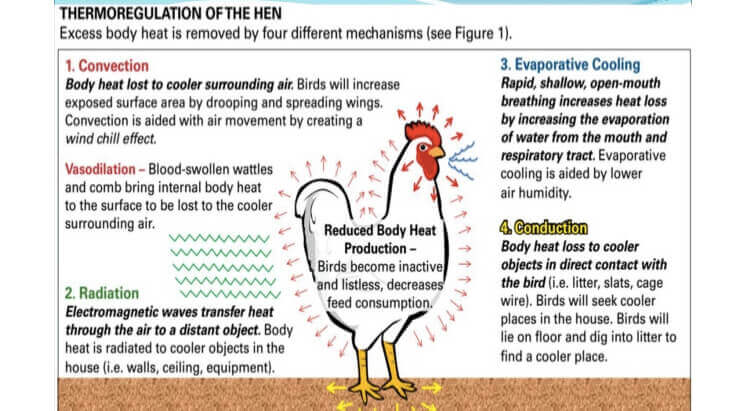

The ability to use vaccines and pharmaceuticals to control the spread of poultry diseases helped expand the large-scale operations, allowing farmers to achieve significant economies of scale and unit-cost reductions. Further, the introduction of evaporation shed cooling in hot climates (e.g. in Thailand) has had a tremendous impact on the industrialization of the sector

Image source: https://image.slidesharecdn.com/poultryfarmingduringhotweather-170521034707/95/poultry-farming-during-hot-weather-7-638.jpg?cb=1495338451

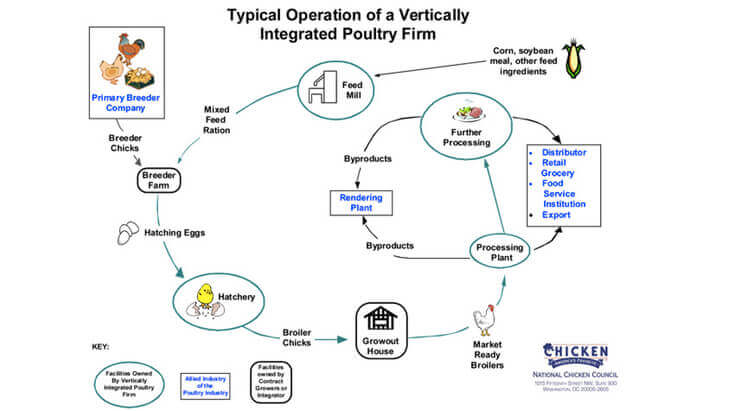

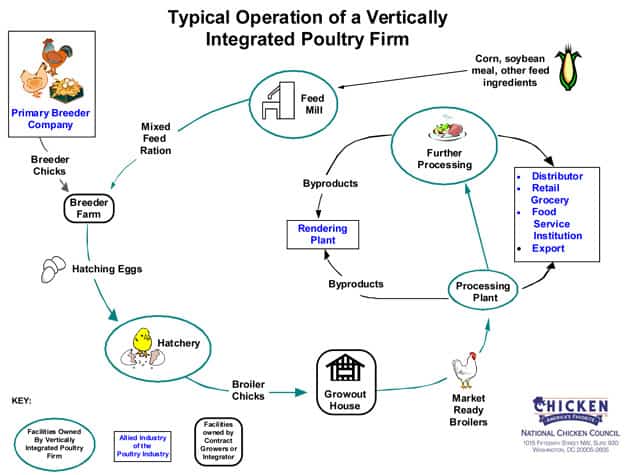

The move towards increased processing of birds into a variety of convenience foods has further accelerated the growth of the poultry industry. Concurrently, there has been a major structural change in the poultry industry throughout much of the world. Specifically, the commercial poultry industry in the developed world and in many developing countries has moved towards large-scale vertically integrated broiler operations that contract grow-out operations to smaller farmers. Today, the commercial poultry industries in most countries are moving towards such large-scale vertically integrated operations. These operations are characterized by a high level of vertical control (ownership) or coordination among suppliers of production inputs, poultry growers, poultry processors and marketers

Image source: http://www.nationalchickencouncil.org/wp-content/uploads/2011/12/Vertical-Integration-Flow-Chart1.jpg)

The specific degree of integration, however, varies among countries and firms. For the most part, integrated poultry operations involve most or all of the following segments: breeding flocks, hatchery, feed mill, production units, assembly of live birds or eggs, poultry slaughtering or packing plants, further processing units, delivery vehicles and distribution centres. Feed mills and further-processing segments are not always included in the integration, although they are an essential part of the production system. In some countries, it was the feed industry which was responsible for the initial integration of the poultry industry. In other countries, it was either the breeding company or the hatcheries which were responsible for the integration. In still other countries, integration was based on the potential market for further processing and fast food, as processors sought to add value to their business and become closer to the final customer. The move towards vertical integration appears to mirror the stabilization of the economy and the growth of the urban market.

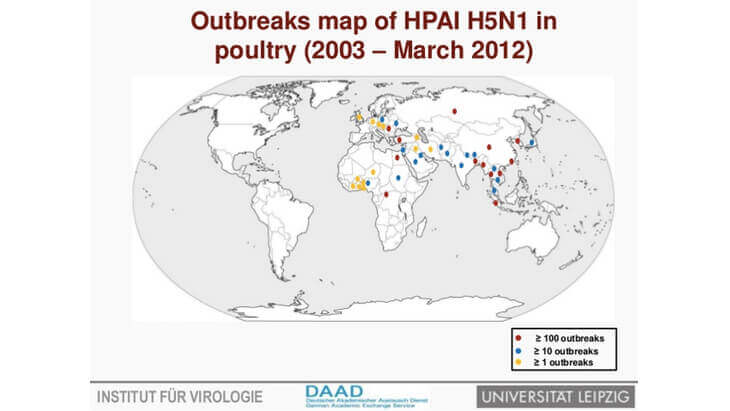

The expansion of these large integrated operations has tended to occur in countries with developing or existing urban markets that supply the major cities. However, in some countries, integrated operations are moving closer to the source of inputs; Brazil is an example. In countries where live chickens are still sold mostly in informal markets, such as India, Indonesia and Viet Nam, forward linkages are also becoming evident, particularly as these countries are faced with the highly pathogenic avian influenza (HPAI) situation and concern is growing about the poultry-to-human spread of the virus (Indonesia and Vietnam). Although there is a move to integrated operations in a number of developed and developing countries, for many developing countries production practices are such that the majority of producers still maintain small flocks which are kept outdoors and are exposed to outside influences. At the same time, these small backyard producers may be interspersed with large-scale commercial operations, giving rise to highly concentrated regions of production near urban areas. Poultry products are among the most perishable, so they have to be produced in close proximity to the demand.

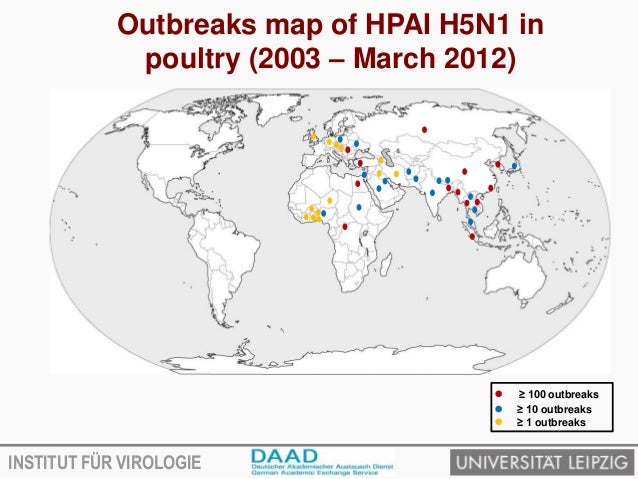

Researchers from the International Food Policy Research Institute, read that In Asia, Latin America and Africa the geographical concentration of poultry operations tends to be around major cities. Poultry distribution patterns can be explained by the distribution of human population, i.e. where there is a dense human population then there is likely to be a dense poultry population. Growing concentrations of animals in large units near cities are associated with greater pollution and increased risk of transmission of both zoonotic and other diseases. Notably, HPAI began in areas with high poultry population density, such as China, Indonesia, Thailand and Vietnam. Increasing concerns over environmental and health externalities associated with concentrated and intensive poultry production near urban areas are causing countries to rethink zoning issues.

Declining poultry prices- Collectively, the changes outlined above have led to a decline in world meat prices over time, particularly for poultry. However, prices are expected to rise as a result of the rising price of maize. Between the 1980s and the 1990s, real prices of poultry declined at a rate of 3 percent per year. This decline continued but at a slower rate. The downward trend in prices was brought about by a number of factors, such as improvements in the efficiency of production of large-scale poultry operations and rapid technological progress, as in the case of the United States of America.

Image source:https://image.slidesharecdn.com/avianinfluenzavirusandtransmission-130207021012-phpapp02/95/avian-influenza-virus-and-transmission-14-638.jpg?cb=1360203074

It is important to note that there was an increase in poultry prices between 2003 and 2004, which could be attributed to a reduction in export supplies caused by several outbreaks of H5N1 HPAI. In 2004/2005, as HPAI outbreaks were reported in some 40 countries previously not infected by the virus, poultry prices noticeably dropped – by 11 percent. Poultry prices are expected to increase over the period 2005 to 2030 at 0.2 percent per year, reflecting increasing demand in China and sub-Saharan Africa, and increasing prices of feed grains such as maize.

Consumers as a whole have benefited from the livestock industrialization process, as a result of reduction in meat prices. It is known that poultry meat and eggs contain protein and micronutrients, such as vitamins from group B, iron and zinc, which could provide an important contribution to the health and nutrition of consumers. For the urban poor, the fall in prices meant an increase in their purchasing power, leading to greater economic access to poultry and other meat. Moreover, especially in the case of poor households engaged in small-scale backyard poultry raising (which is likely to be their main source of animal protein), responding to increased demand probably also leads to higher levels of home consumption.

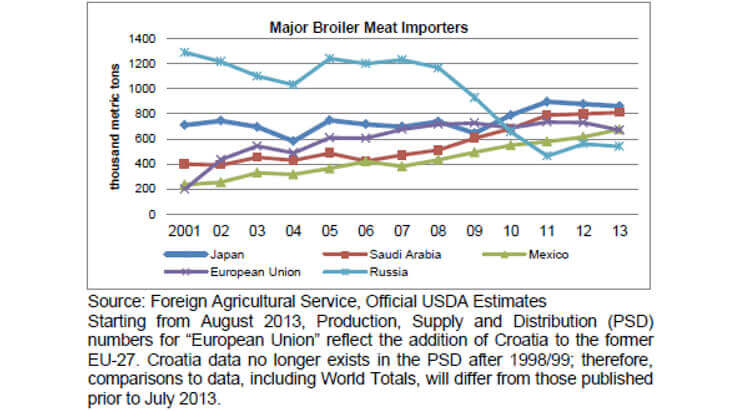

Increased trade in poultry products further increases demand: Broiler products dominate the international poultry trade. The Russian Federation dominates in terms of broiler imports, followed by Japan and the European Union.

Image source:http://www.thefarmsite.com/reports/contents/14-01-22Intgg2.gif

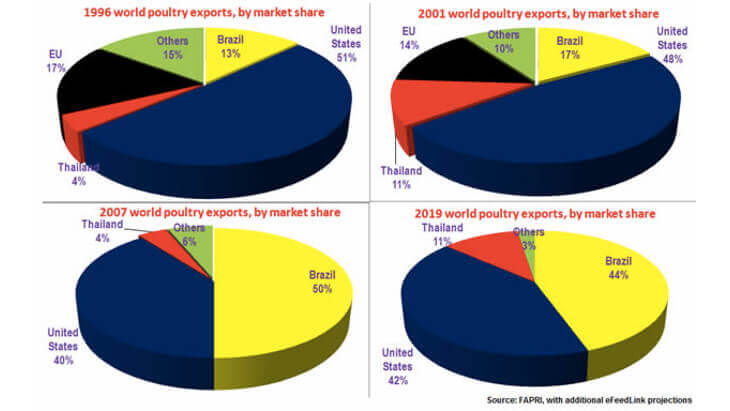

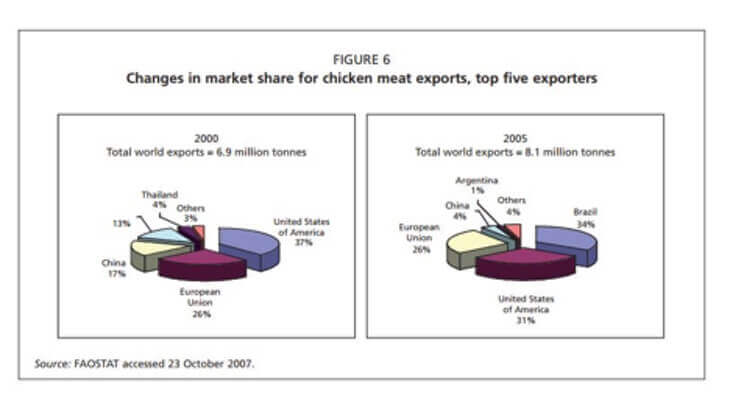

Brazil and the United States of America dominate in terms of broiler exports. China is emerging as an active broiler exporter. Brazil has overtaken the United States of America in terms of chicken-meat exports, expanding by 21 percent from 2000 to 2005, largely due to increases in production and in demand from foreign markets.

Image source:http://www.efeedlink.com/cps/images/2011/january/fbw%201%20focus%201.jpg

The United States of America’s market share of chicken meat exports decreased by 7 percent over the same period, because of lower import needs in the Russian Federation. The United States Department of Agriculture predicts that there will be continued higher demand for Brazilian products because of their competitiveness and aggressive market promotion efforts by Brazilian poultry exporters in new markets. According to FAO 2007 report, trade in poultry meat is projected to increase at a faster rate than production and consumption.

Rise of large-scale retail outlets

The emergence of large-scale retail outlets, including supermarkets and hypermarkets, in developing countries reflect a structural change that alters the way in which meat and dairy products are assembled, inspected, processed, packaged and supplied to consumers.

As a result, livestock markets tend to be divided between the “wet” markets for fresh and warm meat and supermarket outlets for processed, frozen, packaged and branded meat. The relative significance of each market segment is closely linked to the purchasing power of households and individuals, their demand for leisure, their preferences with respect to the form and texture of meat upon purchase, and the relative value or price premium they are willing to pay for a safer product.

Wet markets are still the main output market for live broilers produced by smallholders and independent commercial producers. There are, however, no guarantees that these markets will continue to offer economic opportunities for smallholders over the longer term, even if they are relatively efficient producers, because of large fluctuations in live broiler prices, changing consumption patterns and habits, and the rapid expansion of the large-scale retail sector with its demands for product consistency and known safety.

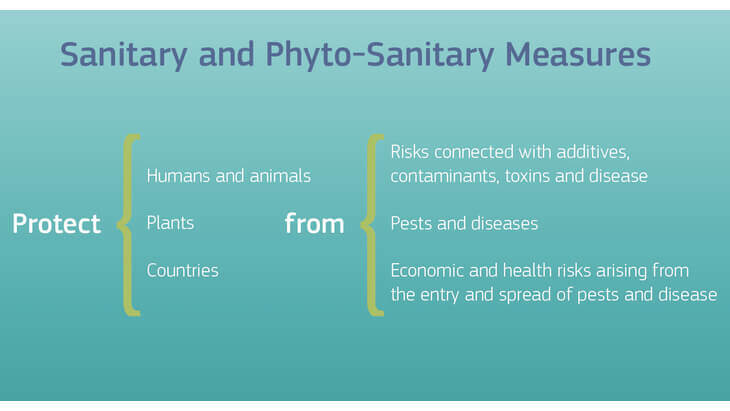

Increased concerns over sanitary and phytosanitary issues and food safety

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Image source:https://ec.europa.eu/europeaid/sites/devco/files/07_sanitary_and_phyto-sanitary_measures.png

{kind=link}

Increasing international trade and globalization are also important drivers of change in the poultry sector. More precisely, they influence the relative competitiveness of producers and production systems in supplying the rising demand for poultry products, particularly in international markets. Increased and long-distance trade requires compliance with standards and regulations and SPS requirements to ensure food quality and safety, as well as public intervention and investment and private costs. Food control and certification systems must be of a high standard. In addition to the health and safety standards and regulations agreed by international bodies (such as the World Organisation for Animal Health (OIE) for animal and human health measures, the Codex Alimentarius Commission for human health measures, and the International Plant Protection Convention for plant health measures), technical requirements may be imposed by retailers. These may include demands for particular meat cuts, carcass size and weight, leanness of meat, egg colour or labelling with particular information or in specified languages.

Large retailers require a reliable supply of agricultural products from their suppliers (producers) with consistency in volume and in quality; hence, they vertically integrate to reduce production risk and transaction costs.

Producers who become part of this integrated chain may face a change in contractual arrangements (e.g. becoming dedicated contract farmers) with increased levels of assistance and higher prices for quality products, but with increased risk if contracts are not met or the retailer closes down. This applies particularly where the farmer must specialize to satisfy volume, safety and quality requirements.

Smallholders can find it increasingly difficult to compete with large-scale producers if they are required to make investments to meet the needs of a retailer. For smallholders to stay involved in this fast-growing segment of the market, they need to integrate into high-value chains through contract farming or other forms of institutional arrangements that have process-based food-safety systems in place and can deliver a form of branding. If smallholders choose to operate independently, it will be harder for them to remain involved over time as markets become more demanding in terms of information about the quality of the product at the time of sale and as market chains become complex.

Changing structure of the industry and supply chains associated with the retailing/marketing of poultry products in developing countries:

Under conditions of clearly specified quality and safety standards, and high risk and uncertainty in output and input markets, vertical integration is a well-known strategy to resist shocks in input and output prices, especially for small producers operating in a market, subject to price instability. It is also an efficient way to provide technical assistance to the producers and to diffuse new technologies. For example, the Charoen Pokphand Group in Thailand has been promoting new housing and manure-management systems over the last six years, resulting in drastic shifts in production among its contract farmers. Let’s take a look at their crisp video to understand how CP chicken products are made:

The introduction of contractual production arrangements within a framework of vertical coordination reduces transaction costs associated with information and secures benefits from market ownership and control over product quality and safety by controlling technical inputs and processes at all levels. Large retailers and large commercial firms in developing countries are increasingly tending towards vertical coordination. All or most aspects of production (from parent stock to processing) are owned or controlled by an individual company known as the “integrator”. Under production contracts, the integrators agree to supply the major inputs, such as day-old chicks (DOCs), feeds, veterinary care and medicines, and technical services. The integrators also arrange for the marketing of live broilers. Integrators bear all input and output price risks and share production risks with the broiler growers. However, the growers typically do not have a share in the benefits of increasing output prices (nor do they share in losses resulting from falling output prices).

Integrators operate in all aspects of production, including raising parent flocks, rearing DOCs and mixing feeds. Conversely, the broiler producers supply the labour, land, sheds, water, electricity and management skills needed for production. They, in turn, receive a growing fee per bird based on performance indicators such as feed conversion ratio, harvest recovery and average live weight. Compensation, additional to the growing fee, is given to growers who surpass the performance standards. In the case of growers who fall below the standards, corresponding amounts per bird are subtracted from the fee. Company field representatives are assigned to visit farms on a regular basis to assist producers with their management and help them to achieve maximum performance and efficiency. Contract broiler farmers have virtually no problem marketing live birds, as the integrators arrange for the lifting of live birds from the broiler farms too. The integrator, who owns the birds, will either sell the live broilers to big wholesale traders or process the birds as chilled chicken to be sold to consumers. In the case of independent broiler growers, output is sold to traders, wholesalers or retailers, or directly to consumers. Lack of negotiating power and lack of access to market information contribute to high transaction costs for independent farmers. Further, lack of facilities for collective action or other institutional arrangements makes it more difficult for smallholder producers to reduce transaction costs. However, overcoming these constraints is not impossible for smallholders if they have the ability and incentives to integrate into a more dynamic private sector business.

Impact of structural changes on profitability of small-scale producers – results from case studies

The main concern with regard to the forces promoting the scaling-up of livestock production in developing countries is that they might drive small-scale producers out of business altogether, and the question of whether the displacement is being accelerated by policy distortions, externalities or structural factors such as transaction costs that disproportionately affect small-scale farms. If true economies of scale resulting from technology, management or transport are driving the incentives for larger-scale poultry farming, then other things being equal, we would expect larger farms to be more profit efficient and have higher or equal unit profits compared to small farms. In such circumstances, the larger farms could eliminate competition from small farms over time by cutting their profit margins. Small farms can stay in business by using family labour valued below market price; this works well in developing countries where there are limited employment opportunities in other sectors. But as soon as employment opportunities in other sectors rise, many smallholder producers will opt out.

Fairoze et al., 2006 findings say that in Thailand, large independent broiler farms made higher profits than medium-sized independent farms. Fee contract farmers in the Thai broiler sample had similar per unit profits at large and small scales. In Brazil, as in the case of Thailand, small and large broiler farms have similar average profits per kg. This may reflect the fact that in the Brazilian case, the majority of small and large-scale farms are contracted to vertically integrated operations. Much of the inputs are supplied by the integrator and in most cases the small and large-scale farms are using similar if not the same technology. Moreover, small-scale farms do not explicitly cost family labour, allowing them to maintain their unit profits close to large farms. There is, however, a growing concern that smallholders might be excluded from the process of contractual arrangements, as integrators would prefer to contract with large-scale farmers so as to minimize production and transaction costs associated with searching for and screening prospective farms, negotiation of contracts, delivery of inputs and services, monitoring of growers’ management on farm, and enforcing contract terms.

Tiongco et al. (2006) observed that an integrator’s transaction costs are incurred on a per grower basis and do not depend on the size of the farm. Moreover, small farms usually require more technical assistance from the integrator per unit of output. For example, a farm visit may require the same amount of time regardless of the scale of production. It was also observed that there was no significant difference between small and large farms in terms of the growing fees paid by integrators per unit of output. Holding the growing fee per unit constant, integrators would rather contract with larger producers to lower their cost of procurement or to lower the cost of default.

Smallholders will have at least a chance to compete with larger-scale producers, as they have the ability to produce at a lower per unit cost of production or at least achieve profits per unit of output that are similar to those of large-scale farmers. If smallholders are not able to sustain a rate of productivity growth equal to or greater than that of large farms under these conditions, they will have a hard time remaining in business.

There are, basically, five elements that are essential to ensure smallholders’ access to markets. First, producers need access to extension services or technical assistance so that they stay up to date with the specialized techniques needed to ensure the safety of high-value products. Second, they need access to good infrastructure so as to be able to manage flows between chain links quickly, so as to meet the rigid deadlines imposed by buyers and reduce transportation and distribution costs. Third, they need access to good sources of information so as to be well informed of changing market demands and to be able to integrate this information rapidly across the supply chain. Fourth, producers need to have the ability to produce products that are certifiably safe and of good quality. Certification systems need to be not only consistent but also credible, to meet buyer and customer demands. Lastly, producers need to have good mechanisms for coordination of their supplies to the markets so as to ensure the timely delivery of high-quality products. If market failures are preventing smallholders’ access to these important elements, it is very possible that they will lose much of their current market access unless some sort of institutional arrangement can be made to address the problems.

This was an analysis of the Poultry Industry. If you would like to have a detailed discussion, please get in touch with us at hello@pixelsutra.com. We would be glad to assist you.